The Challenges of Anti-Money Laundering

Enforcement actions and penalties for non-compliance with anti-money laundering (AML) regulations are on the rise. Fines for AML, data privacy and MiFID have risen 27% in 2020. US regulators have historically been the toughest enforcers of AML rules, but in 2020 APAC overtook the US in the value of enforcement actions and there has been an increased focus on penalizing individuals, rather than just financial institutions. At the same time banks are likely to get squeezed even further if the US implements a proposal to lower the suspicious transaction threshold from $3,000 to $250. This will force banks to significantly increase their investment in AML operations to manage the growing number of investigative cases.

Compliance teams are already fighting to keep up with the increasing volume while under immense cost pressure and saddled with outdated technology.

At the same time bad actors are employing an increasingly diverse set of strategies to stay ahead of regulators and compliance departments. This includes shifting activity towards the non-bank financial sector or taking advantage of the anonymity that comes with digital currencies, virtual assets, custodian wallets, and pre-paid cards. If the situation was not complex enough, the COVID-19 pandemic has wreaked havoc on banks’ transaction monitoring and related AML compliance capabilities.

Security protocols and the associated infrastructure for banks was developed for a world where compliance and AML operations were run from within the physical confines of a bank’s office, not for the current necessity of employees accessing servers remotely from their homes.

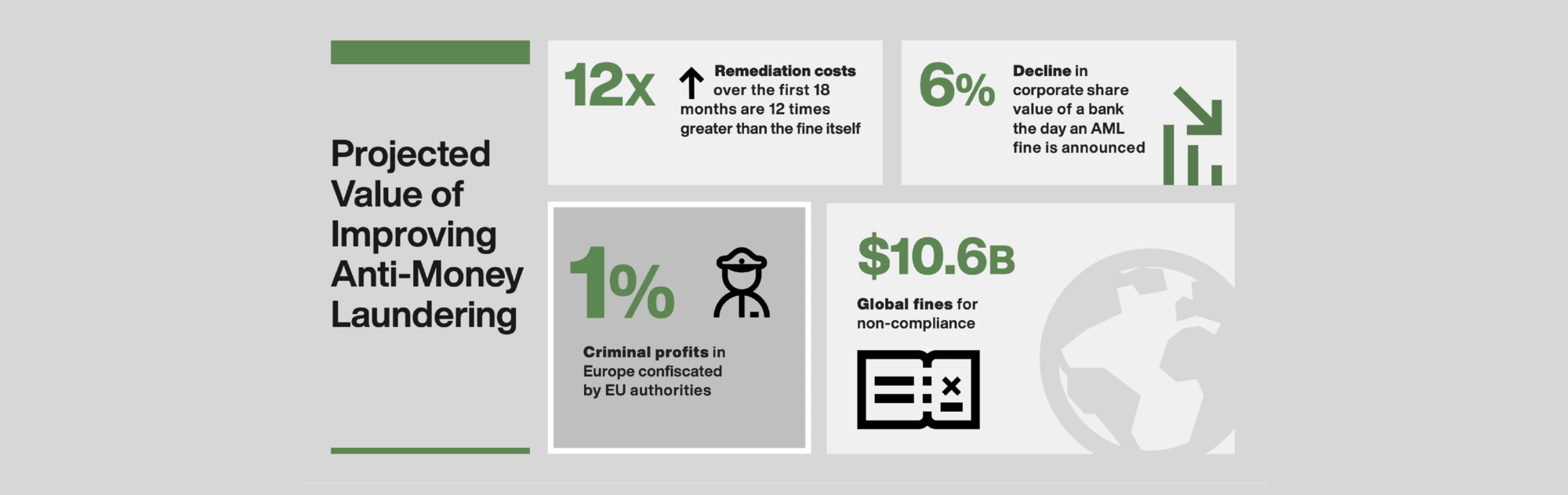

Figure 1: Projected value of improving Anti-Money Laundering 1, 2, 3

1. How Europe Can Fight Anti-Money Laundering, 2020 2. Financial Institution Fines, Fenergo, 2020 3. Anti-Money Laundering Controls Failing to Detect Terrorist Cartels and Sanctioned States, March 2018

Traditional rules-based AML software create an excessive amount of alerts that require review and disposition by compliance investigators. Not only are these investigations painfully long, require navigating the multiple systems of a typical bank, but are often fruitless, with over 95% of the alerts proving to be false positives.

Regulatory demands for increased money-laundering scrutiny are on the rise and so are the associated costs of AML operations. In response, banks need to reimagine their AML operations with greater automation and apply a different approach for identifying and investigating suspicious activity.