JOE FIORICA, GLOBAL HEAD OF EQUITYSTRATEGY, CITI PRIVATE BANK WIETSE NIJENHUIS, EQUITY CLIENT PORTFOLIO MANAGER, CITI INVESTMENT MANAGEMENT

While economic shutdowns represent a widespread threat to dividends, the value of dividends and the companies that can sustain them has risen. We favor companies from certain industries that combine solid track records of dividend growth and resilient business models.

KEY MESSAGES

Unprecedented economic shutdowns are calling into question the sustainability of dividends, as well as share buybacks. Companies in certain industries could be forced to preserve their cash, at least until there is more clarity around the length and depth of the economic downturn. This even includes some enterprises that grew dividends throughout the Global Financial Crisis of 2008-09.

In these unprecedented times, we are seeking out companies whose balance sheets and cash flow previously gave them the scope to do share buybacks in normal times. We think these companies are more likely to be able to maintain their dividends. Certain parts of the tech sector stand out here, as many technology businesses have been less impacted by the economic effects of social distancing. In the case of the healthcare sector, ample free cash flow has tended to finance buybacks and mergers & acquisitions activity. Both could be scaled back to maintain dividend payouts.

Meanwhile, as the worst-hit industries focus on survival, they are likely to cut buybacks, dividends, and expenses deeply. The energy and travel & leisure sectors stand out, especially those constituents that have been borrowing to meet dividends. As the second largest buyback sector after tech, the banking industry’s ability to maintain dividend payments looks solid at first glance. Banks' balance sheets are much stronger today than they were going into the 2008-09 crisis.

However, banks are inextricably linked to the economy’s health and to government policies that might constrain their financial flexibility. Therefore, if corporate and consumer delinquencies grow despite government support, banks could see material balance sheet impacts, including major reserves for credit losses. We expect this worstcase scenario to be avoided, but close monitoring of threats to banks’ payouts is vital.

Regionally, we see Europe at greater risk of dividend cuts than the US. Current dividend yields are higher and share repurchase buffers are lower, especially in the financial and energy sectors, the former being the region’s largest sector. After a decade of weak profitability, Europe’s banking system is much less healthy than its US counterpart. Indeed, its banks have already announced widespread dividend suspensions. Political pressure to focus on supporting employment over dividends is greater in Europe.

Seek growing, sustainable dividend yields

Over time, reaching for high current yield can be risky. Such strategies often include investments in companies in danger of cutting dividend payments. These companies offer temptingly high yields, but have balance sheets that cannot sustain them. We prefer “dividend growers,” companies that have consistently grown their dividend payments over time, demonstrating fiscal discipline to do so – see Realigning income portfolios: Go for growers in Outlook 2020. Many did so even during the 2008- 09 financial crisis. These firms’ dividend payments represent a sustainable proportion of profits, without a need to maximize payouts or assume unsustainable debt to pay them.

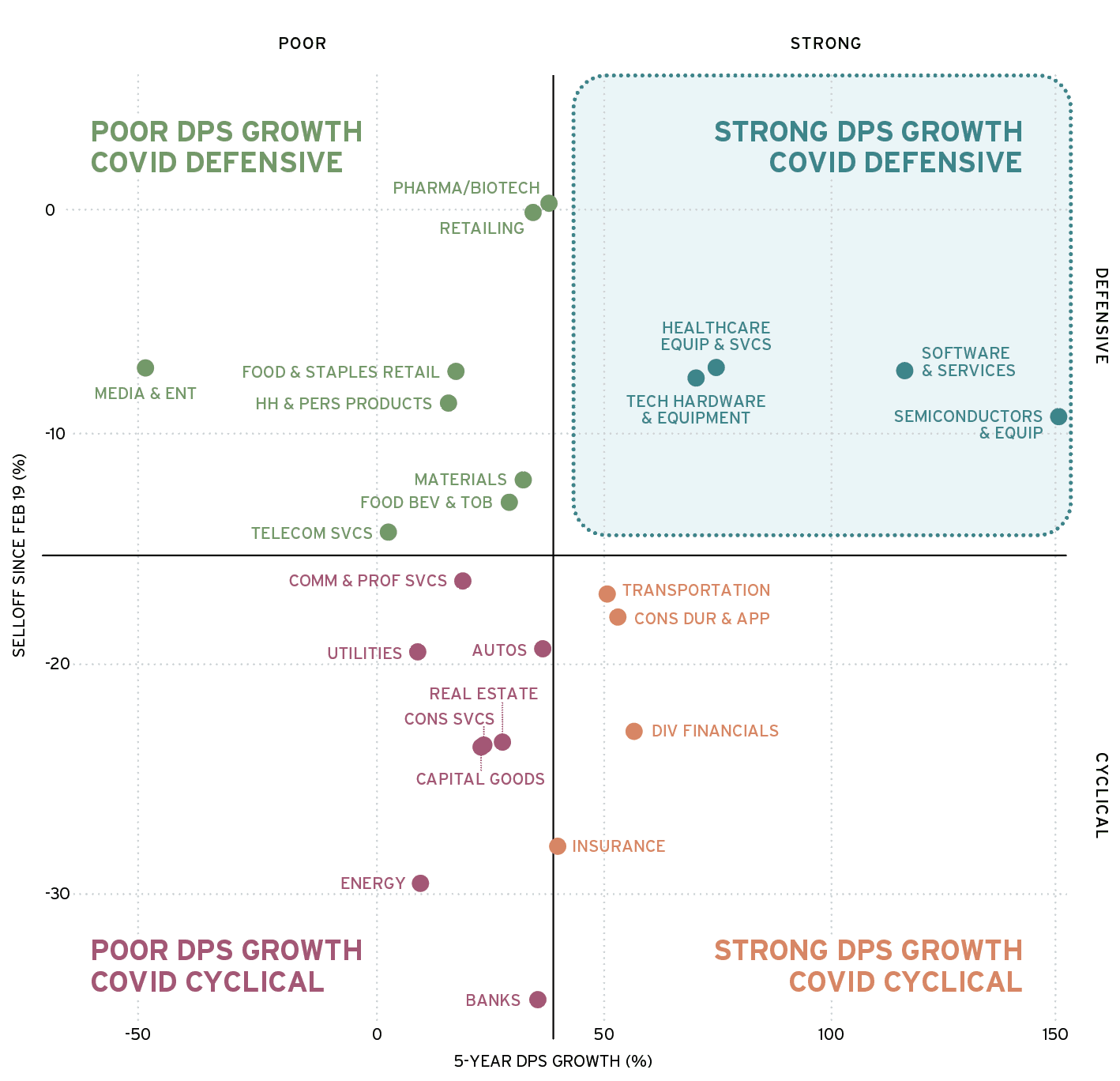

The combination of a track record of growing dividends, a resilient business model, and being in the “right” industry is likely to prove the best guide for identifying those likeliest to sustain dividends through this crisis. We note that since February’s market peak, dividend growers in more insulated industries have outperformed the market – figure 1. Given the unique nature of the current environment, active managers may be better poised to identify such firms than purely passive strategies based solely upon historical dividend growth.

Source: Factset, through 19 May 2020. Past performance is no guarantee of future returns. DPS is dividends per share. We define COVID defensives and COVID cyclicals as sectors whose business models have proved more resilient and more vulnerable respectively during the pandemic. See Glossary for definitions.