STEVEN WIETING, CHIEF INVESTMENT STRATEGIST AND CHIEF ECONOMIST

Our key investment themes and recommendations have performed well amid COVID-19. We continue to emphasize their long-term importance to portfolios.

KEY MESSAGES

Unstoppable trends are COVID-immune

As the global prevalence of COVID-19 started to become clear in February, Citi Private Bank reduced its allocation to equities, adding instead to US Treasuries and gold – see Investing in a new economic cycle. We also advised directing new investment dollars towards industries that were likely to be least impacted by the peculiar phenomena of economic shutdowns and social distancing. Unsurprisingly, this included many industries that we were already recommending as part of our Unstoppable Trends theme.

We define unstoppable trends as powerful longterm forces that are revolutionizing the ways we live and do business globally. These trends can endure throughout an economic cycle – and in the case of a pandemic, see an acceleration of their drivers, offering resilient growth potential to portfolios. Our trend of Digital disruption considers how digital innovation is revolutionizing companies and industries. The rise of Asia addresses the steady shift in global economic power from West to East. Increasing human longevity explores how the aging of the world’s population will impact demand patterns, especially for healthcare. All of these trends are likely to last for two decades or more.

Source: Haver, as of 20 May 2020. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. Past performance is no guarantee of future returns. Real results may vary.

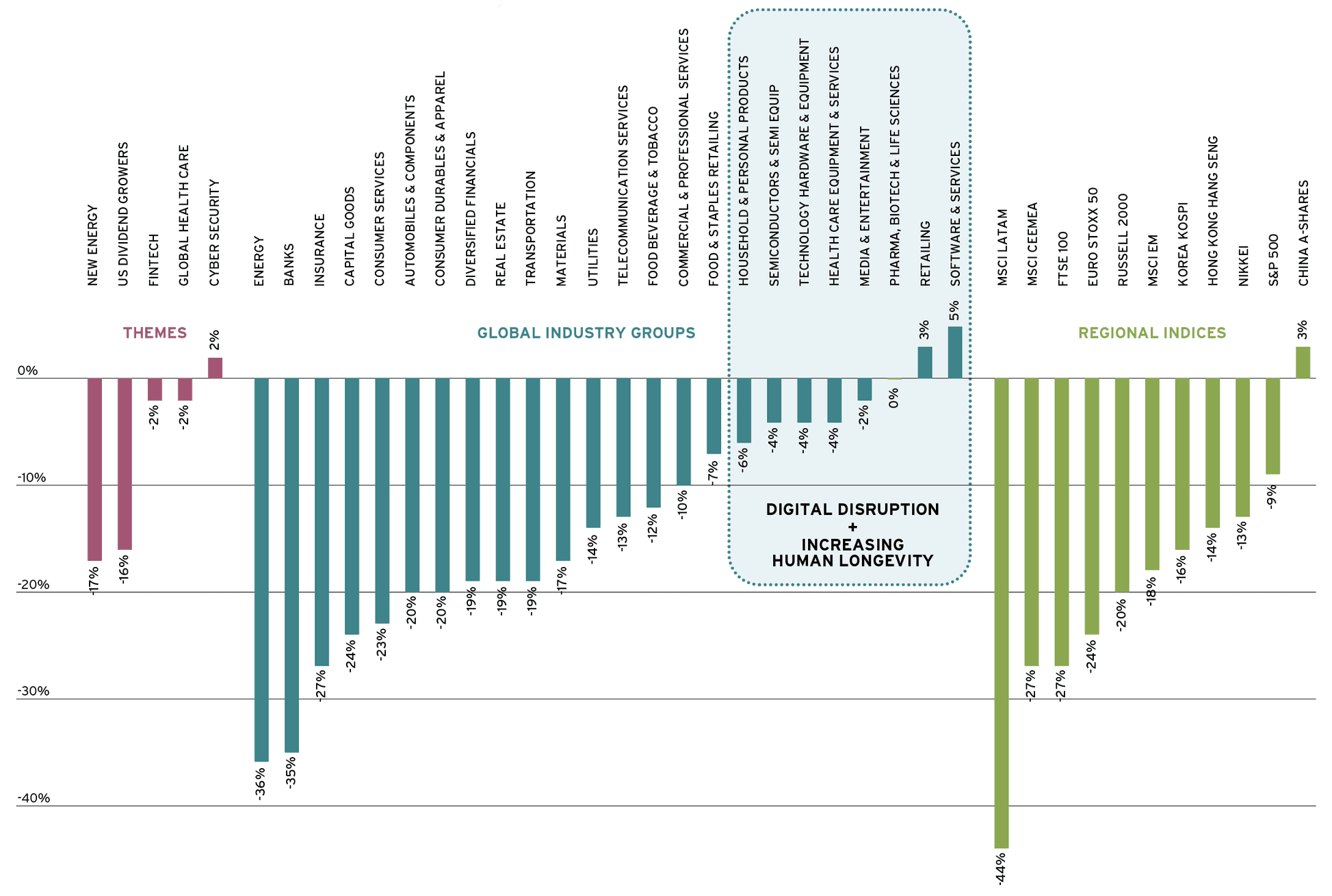

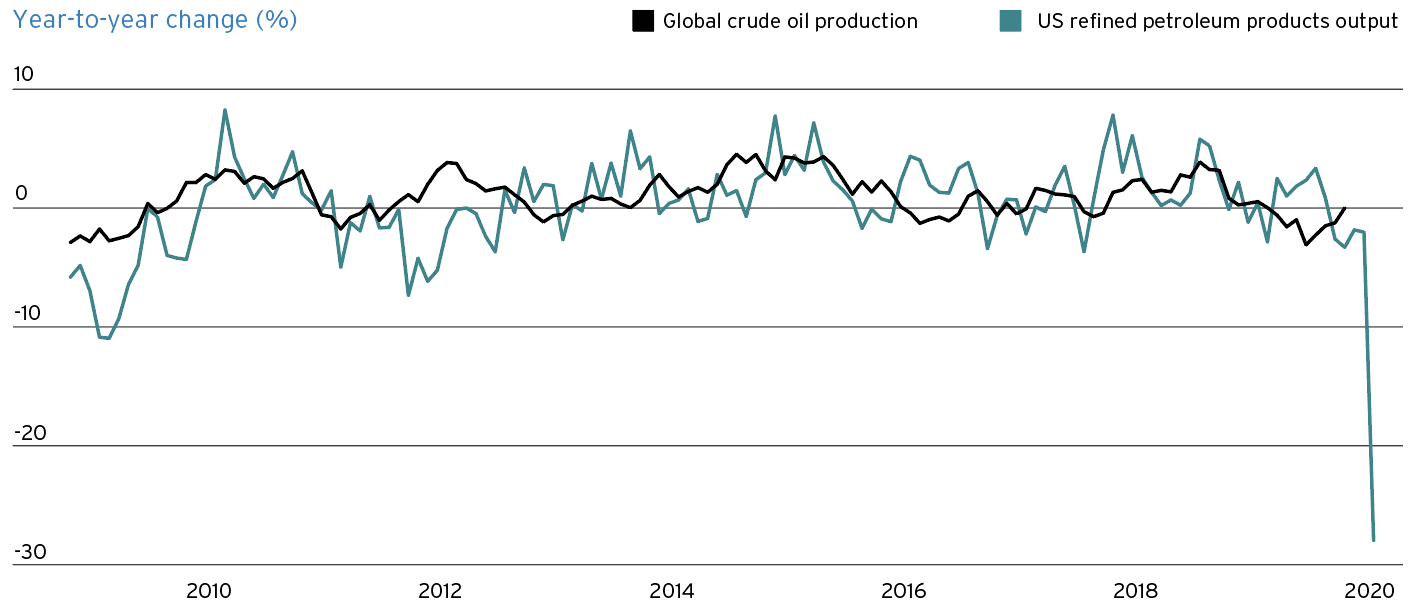

Some sectors and companies related to these trends have been among the strongest performers of 2020 so far – figure 1. Digital disruptors in software, e-commerce, and digital media have not only managed to outperform a falling market, but also register absolute gains. China – a key element within both The rise of Asia and Digital disruption – has also outperformed. Its large domestic tech sector and its early recovery from the pandemic helped drive good year-to-date results. Along with IT industries, healthcare – our Increasing human longevity theme – has outperformed as one might expect amid a pandemic. Traditional energy – the secularly challenged sector whose vulnerability to sustainable alternatives we highlighted in The future of energy – has been the worst performer year-to-date. The collapse in demand for transportation fuel has deepened the fossil fuel industry’s slump that we described as “gradually unfolding” in Outlook 2020 published at the end of last year – figure 3.

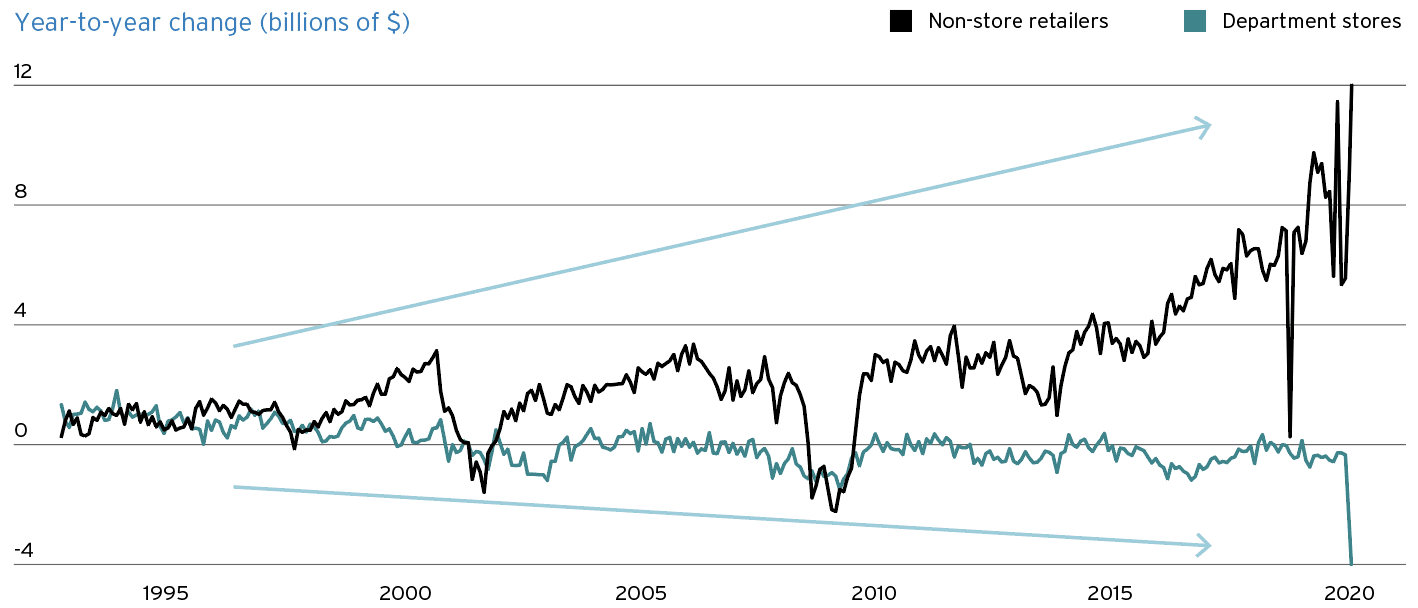

We believe that the experience of COVID-19 – and the post-pandemic outlook – is likely to add further momentum to these Unstoppable trends. Here are some examples. E-commerce has become even more dominant at the expense of traditional retailers, such as department stores – figure 2. As fifth generation (5G) wireless networks continue to roll out over the next few years, we expect the uptake of digital content and other services to increase still further.

Source: Haver, as of May 2020.

Source: Haver, as of May 2020

We remain confident in the long-term growth prospects of our Unstoppable trends. Despite their recent strong performance, we would not divest investments related to these themes. Since last March, however, we have gradually broadened our preferences to include recovery prospects, rather than just assets that would better withstand the COVID-19 turmoil. Exposure both to Unstoppable trends and industries, sectors, and countries most likely to recover more quickly than expected is a powerful portfolio combination, in our view. (Note: To make room for “recovery” investments, we will underweight some of the regional investments likely to be most challenged or limited in their recoveries.)

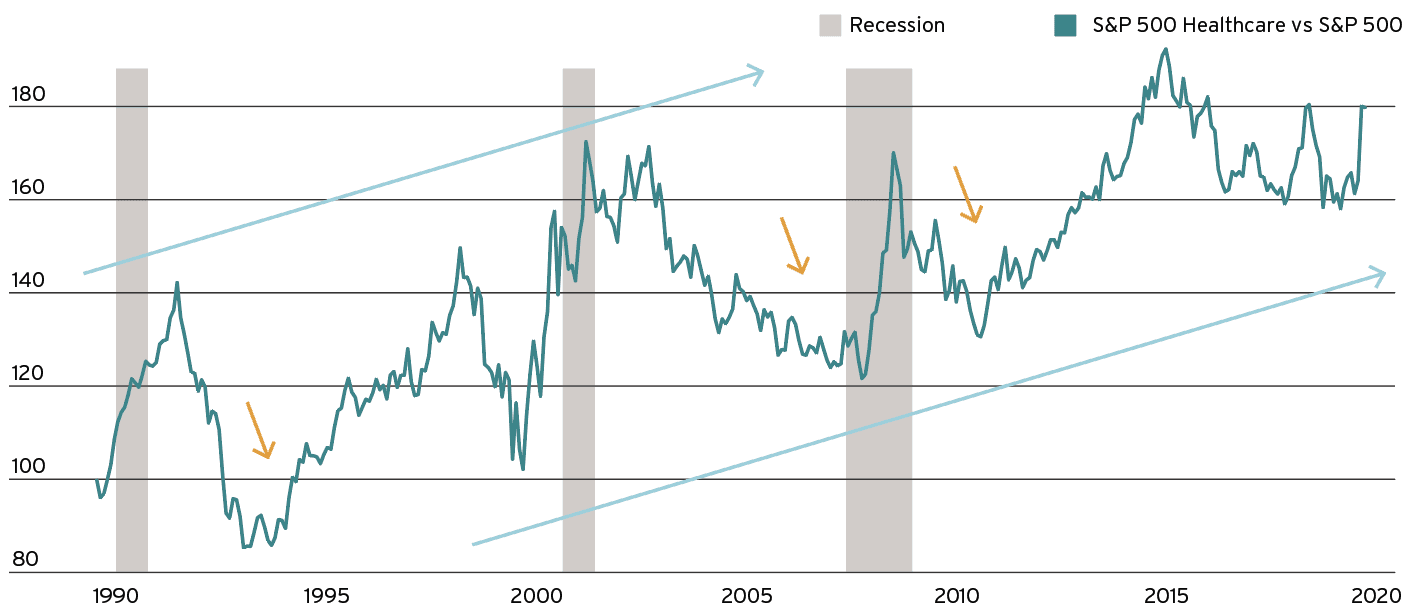

Healthcare – a favored sector of ours – has a consistent record of revenues and earnings growth throughout cycles. However, it has tended to underperform in the early years of new economic cycles – figure 4. As our tactical investment allocations evolve, we will make sure not completely to exclude investments that have suffered the “COVID collapse” – see Investing in a new economic cycle.

Source: Haver, as of 20 May 2020. Index rebased to 100 as of 1 Jan 1990. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only.

Identifying yield alternatives

In Outlook 2020, we suggested avoiding very low or negative yielding bonds and seeking income instead from various other investments. This advice is even more relevant today. We therefore reiterate our recommendations to allocate to the highest quality dividend growers – see Seek sustainable dividends – as well as to select fixed income assets that still offer yield – see Cash is not king. We also continue to advocate income-producing capital markets strategies for qualified investors – see What smart families are doing in capital markets.

Joe Fiorica also contributed to this article.