STEVEN WIETING, CHIEF INVESTMENT STRATEGIST AND CHIEF ECONOMIST DAVID BAILIN, CHIEF INVESTMENT OFFICER

The COVID collapse and policy response have profoundly affected our Strategic Return Estimates, asset allocation strategy, portfolio construction, and tactical market recommendations. We are entering a new economic cycle and this demands a new approach to investing.

KEY MESSAGES

The COVID collapse in the economy was caused by an exogenous shock that collapsed world business activity

The COVID-19 pandemic ended the longest economic expansion in history. The 128 months from June 2009 to March 2020 was a period of modest growth for the world economy following the Global Financial Crisis.

Now, we begin a new economic and financial market cycle.

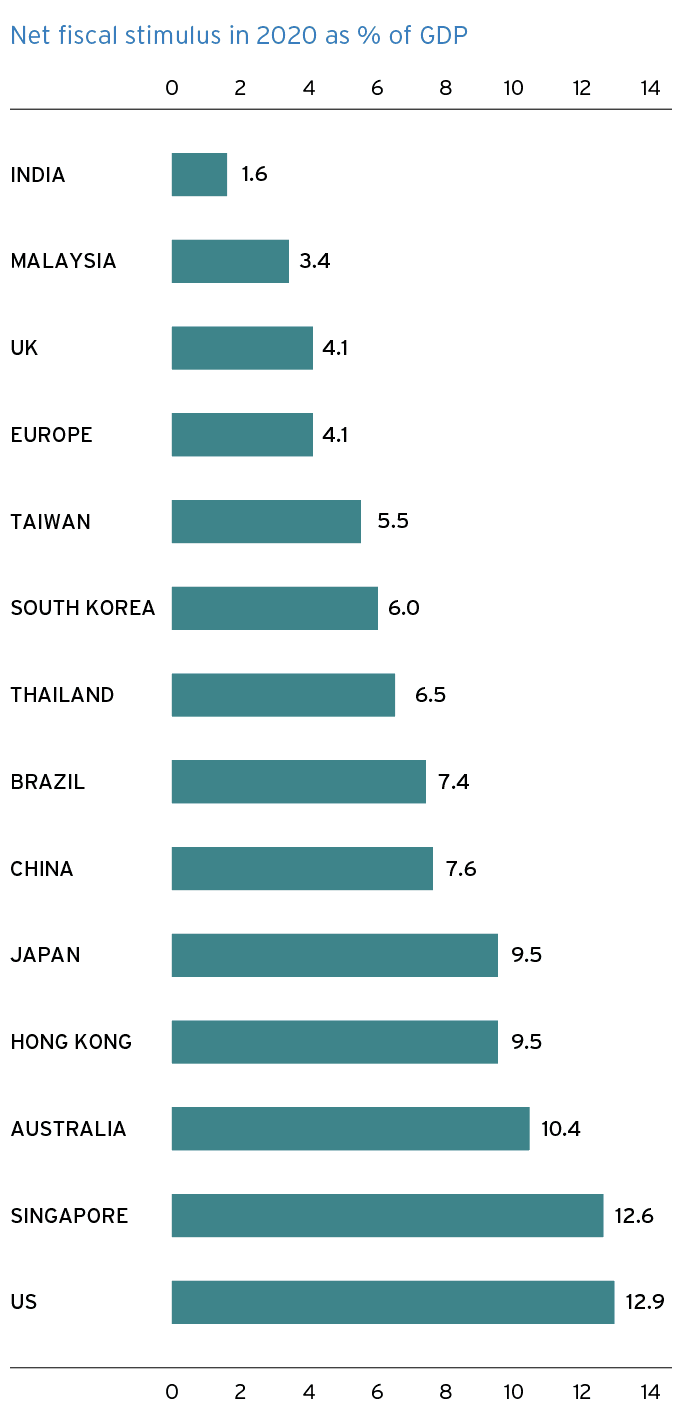

The COVID collapse was caused by an exogenous shock that shut down world business activity. But unlike 2008, governments worldwide were swift and decisive in spending current and future resources to build a bridge to economic recovery. Globally, policymakers will deliver $6 trillion in current-year spending, while central banks have embraced open-ended asset purchases of an equivalent amount. As figure 1 shows, the US is leading global stimulus efforts, with roughly half the world’s fiscal and monetary easing in the US dollar. The Federal Reserve also cut US policy rates back to zero, pledging to keep them there until labor markets “normalize.” These anticipatory actions will serve as the starting gun for a recovery that will begin in the third quarter of 2020.

Source: FactSet and Citi Research through 12 May 2020.

A rapid economic contraction of this severity and speed would normally elicit equally bearish sentiment from backward-looking investors. But the level of fiscal and monetary stimulus was so massive that it brought confidence to investors willing to look beyond the deep chasm. Markets responded with a recovery that confounded pundits and experts alike.

Whereas prior recessions allowed time for appreciated bonds to be liquidated and exchanged for depressed equities, this one has not. Even Warren Buffett could not put Berkshire Hathaway’s huge cash pile to work quickly enough. Clear market leadership by technology companies – those least negatively impacted by the economic shutdowns – provided a catalyst for the market rebound. The speed of the equity market recovery will require investors to make faster and bolder investment decisions. We think the quality of these decisions may significantly shape your performance for the coming decade.

While markets jumped higher and faster than in any prior post-recessionary period, investors were discerning. Defensive equities rose and cyclical equities fell disproportionately, punishing industrials and banks, to name just two sectors. Some overseas markets were similarly hit hard. So, as we reflect on what is different this time, the new economic cycle demands a tactical approach. We will need to allocate between particular market segments and regions over time.

We will need to expose client portfolios to parts of the market, like small- and midcap equities, as the recovery takes shape. In short, the new economic cycle will require new approaches to everything from security selection to portfolio construction to asset allocation.

The path of decline and recovery: An inevitable rise

Shutting down whole economies has produced history’s fastest economic collapse. We estimate the annualized pace of decline in second quarter US GDP may be 35%-40%. A drop this large distorts the math of recovery, as gains and losses are asymmetric. For example, we expect only half of those unable to work in the second quarter across western economies will be able to return to their jobs in the third quarter. We estimate this partial rebound alone is likely to result in GDP growth of 25%-30%. As you can see, the numerical growth will look large, but only just begin filling the employment hole.

In terms of consumer spending, we can look overseas for clues as to how the recovery might look in the West. The path of Chinese auto sales is one such data point. As China’s economy shut down, auto sales fell 83% in February. As Chinese workers now fear using public transport, auto sales quickly exceeded their pre-COVID pace by April. While March saw only part of this two-month recovery, the monthly gain was 240%.1 Other clues are likely to emerge. For example, Germany’s Lufthansa is rapidly expanding intra-European flights. In all cases, the ensuing sector recoveries will likely be significant, but fall well short of full recovery.

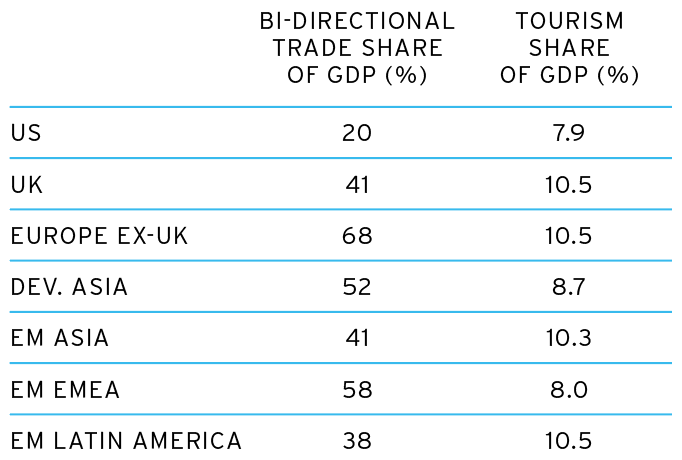

Importantly, certain countries and regions are unable or unwilling to provide economic stimulus. Some of them will suffer deeper shocks owing to their dependence on international tourism, exports or both – figure 2. Emerging markets with high external borrowing requirements, those that borrow in foreign currencies or have pegged currencies are more vulnerable, as they have the ability to steer their economies to higher ground.

Source: FactSet and Citi Research through 20 May 2020

The Eurozone lagged the US during the recovery after the Global Financial Crisis of 2008-09.2 With a greater trade and tourism shock and less fiscal stimulus, the Eurozone should expect a 2020 growth decline nearly twice as large as that in the US. Along with greater demographic constraints and more slower-growing industries, an inadequate level of regional support for the most COVIDimpacted Eurozone countries is likely to result in a weaker regional recovery for several years to come.

We also see oil-producing states as likely to experience sustained pressure. We expect production cuts and a modest resumption of travel to boost oil’s price toward $40 by year-end. But oil is unlikely to regain pre-pandemic levels due to a long-term secular shift away from fossil fuel consumption, increased US supplies, and a technology revolution in alternative energy.3

MSCI Indices in all cases, except for S&P. Source: Bloomberg through 20 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. See Glossary for definitions.

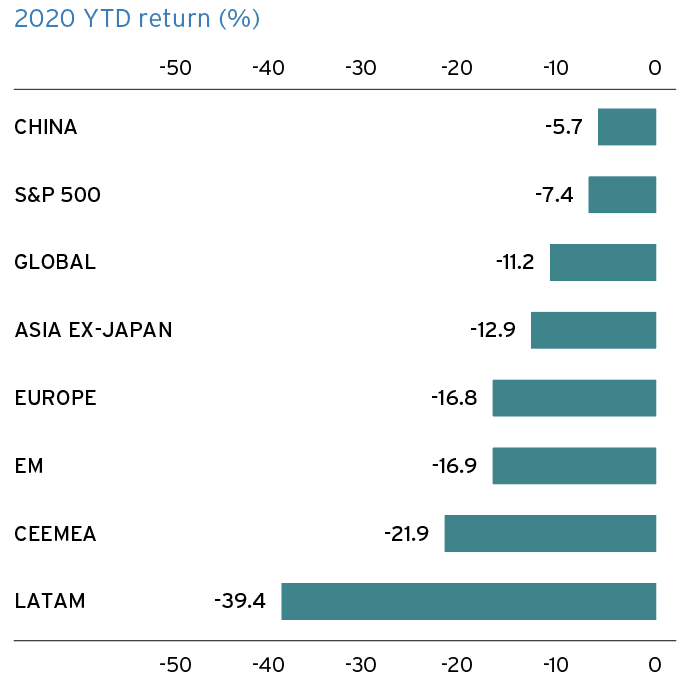

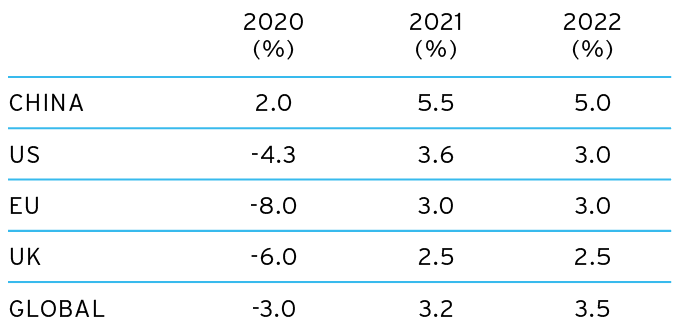

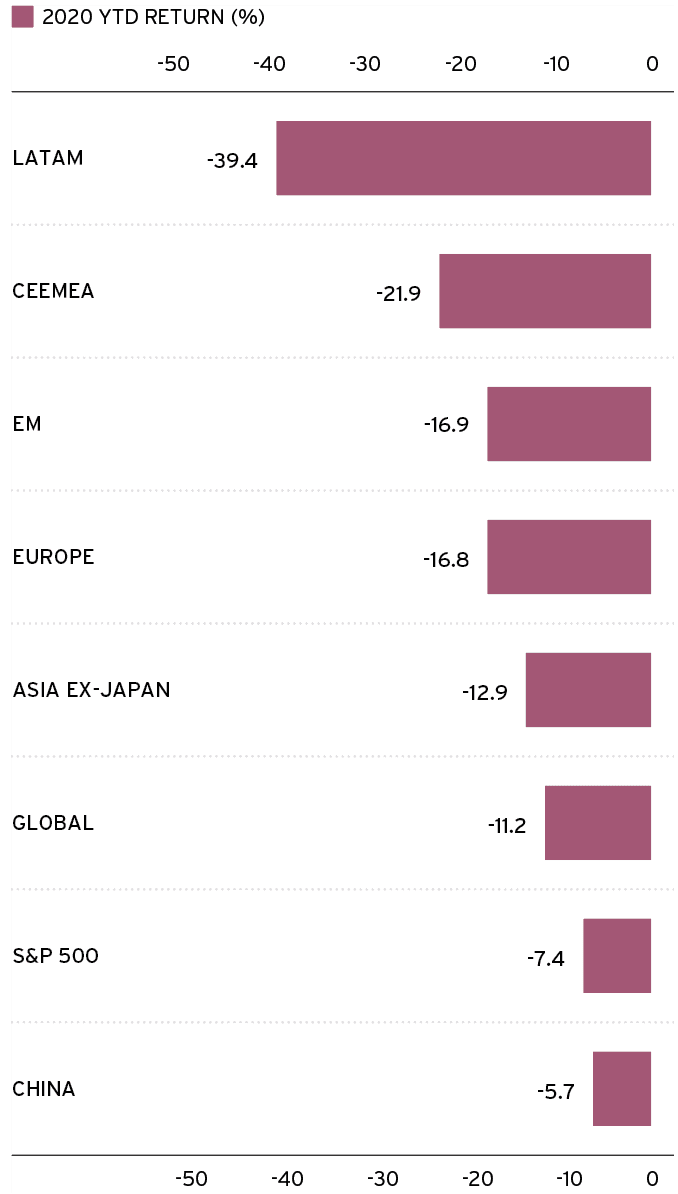

Our economic assumptions are already significantly reflected in regional financial returns so far in 2020 – figures 3 and 4. Our goal will be to assess which regions and markets are over- or underestimating the recovery going forward.

Source: Office of the Chief Investment Strategist, Citi Private Bank, as of 20 May 2020. All forecasts are expressions of opinion and are subject to change without notice and are not intended to be guarantees of future events. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. Past performance is no guarantee of future results, actual results may vary.

Seeing the dispersion in markets as an opportunity

We believe today’s massive dispersion in potential returns between regions, industries, and companies represents the biggest opportunity for investors at the inception of this recovery. We will guide investors on the opportunities and their sequencing. For discretionary investors, we will reallocate portfolios accordingly. And for opportunistic investors, we think you will need to act decisively, as adding the appropriate exposures at the right time may improve future returns. Likewise, failure to act may well hinder your subsequent portfolio growth.

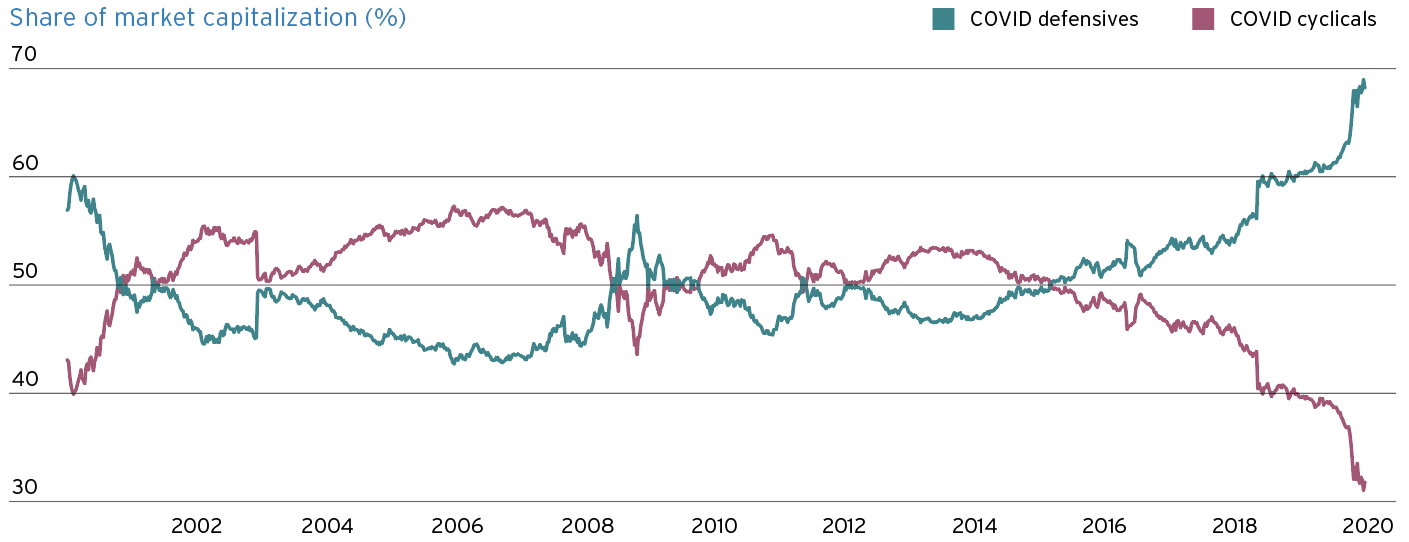

As the crisis unfolded, we rapidly saw that “COVID defensives” – our label for US sectors including information technology, e-commerce, healthcare, and staple industries – massively outperformed beaten-up “COVID cyclicals” – our label for industrials, energy, financials, and real estate – figure 5.

Source: Bloomberg through 5 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. COVID cyclicals: Financials, industrials, energy, materials, real estate, consumer discretionary ex-Amazon COVID defensives: IT, healthcare, communication services, consumer staples, utilities, Amazon

In our view, this outperformance is unsustainable and presents an investment opportunity. Market leadership by companies less impacted by the economic shutdown makes sense, but the degree to which they have appreciated relative to the poor performance of industrial companies does not.

Given the exogenous nature of the shock and the rebound off the bottom, consumer and business confidence were not dashed as much as one might expect. Hence, we expect spending in industrials will do better, as will those equities over time.

Build portfolios for 2021 and beyond, not 2020

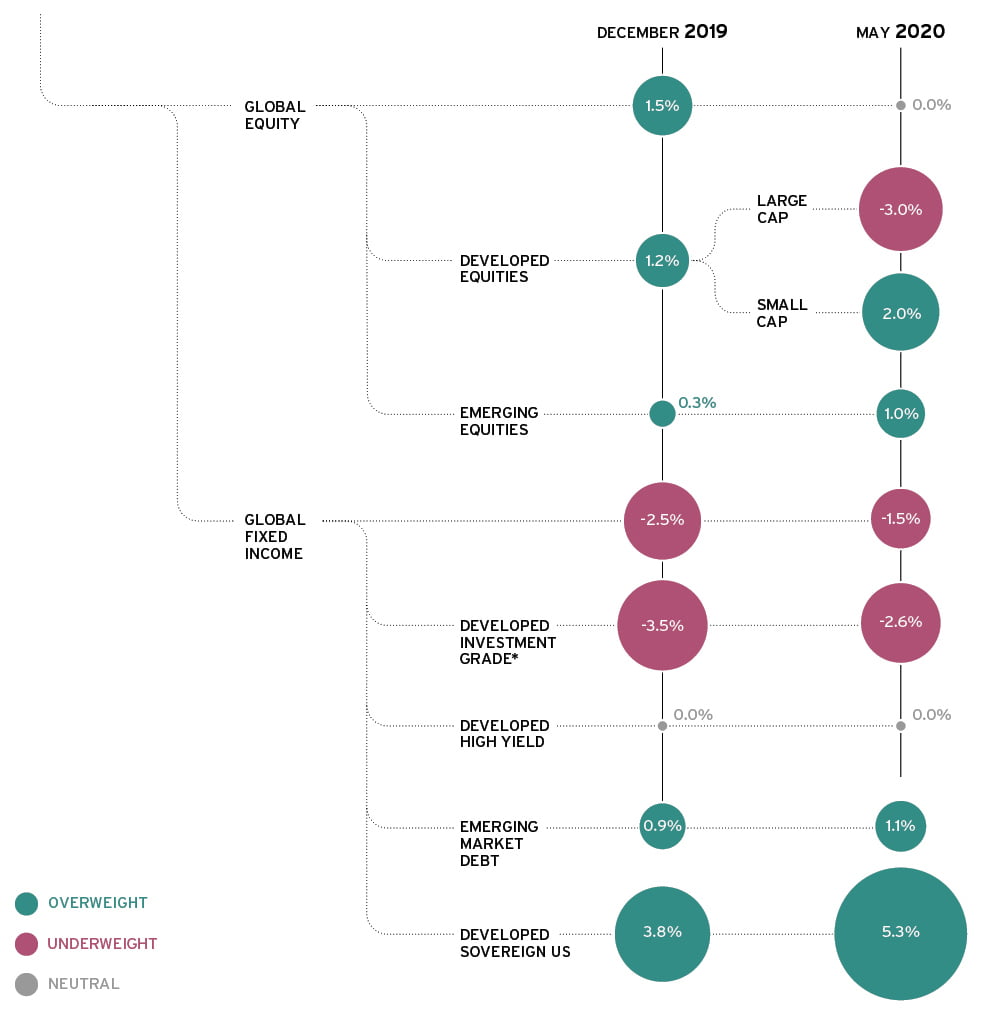

Our new Strategic Return Estimates show major changes as we enter the new cycle. Importantly, the portfolio value of fixed income broadly has fallen. With the exception of EM debt and some parts of the high yield market, lower interest rates pinned near zero have reduced bonds’ diversification value and their long-term return prospects even more so – see Major changes to our Strategic Return Estimates. We therefore need to consider other ways to seek diversification4 and returns. In equities, the performance of indices is not the story. There are sub-sectors that will be more valuable as portfolio components.

With the global economy still shrinking, equity investors have largely taken the wise leap to believing in eventual recovery. Consequently, broad risk asset pricing does not offer outsized prospective returns. Yet, it is possible that a future equity setback could change that. While broad equity markets mostly rise and fall together, the relative value of markets and their future prospects will play out in unexpected ways. Europe faces great risks, but also has scope to recover, if policymakers show unity and resolve. For now, however, we are underweighting equities across the Eurozone and the emerging markets (EM) of Europe, the Middle East and Africa. This includes Eurozone government bonds, where we also remain underweight.

Oil markets will also continue to experience boom and bust. Following the present bust and likely recovery, it will still be a great challenge for oil-producing states to diversify their economies enough in a world where oil demand is waning – see The future of Energy in Outlook 2020.

Also at the heart of our new cycle investment strategy is increasing exposure to attractively valued investments with the potential to generate income – see Seek sustainable dividends – and long-term growth opportunities. We also want to add exposure gradually to depressed assets that will be deemed undervalued a year or more from now. By contrast, we will reduce exposures in regions and sectors whose recoveries will likely lag – see Our favored markets.

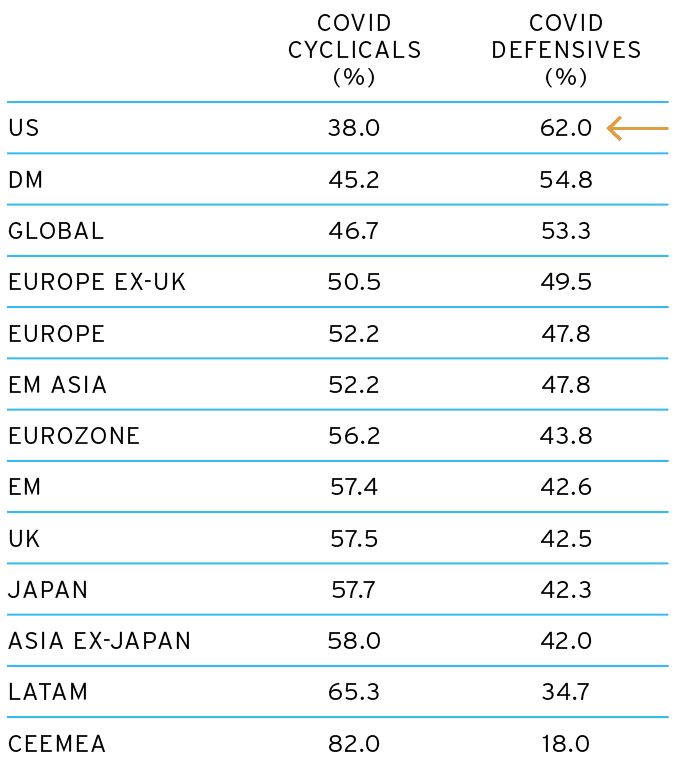

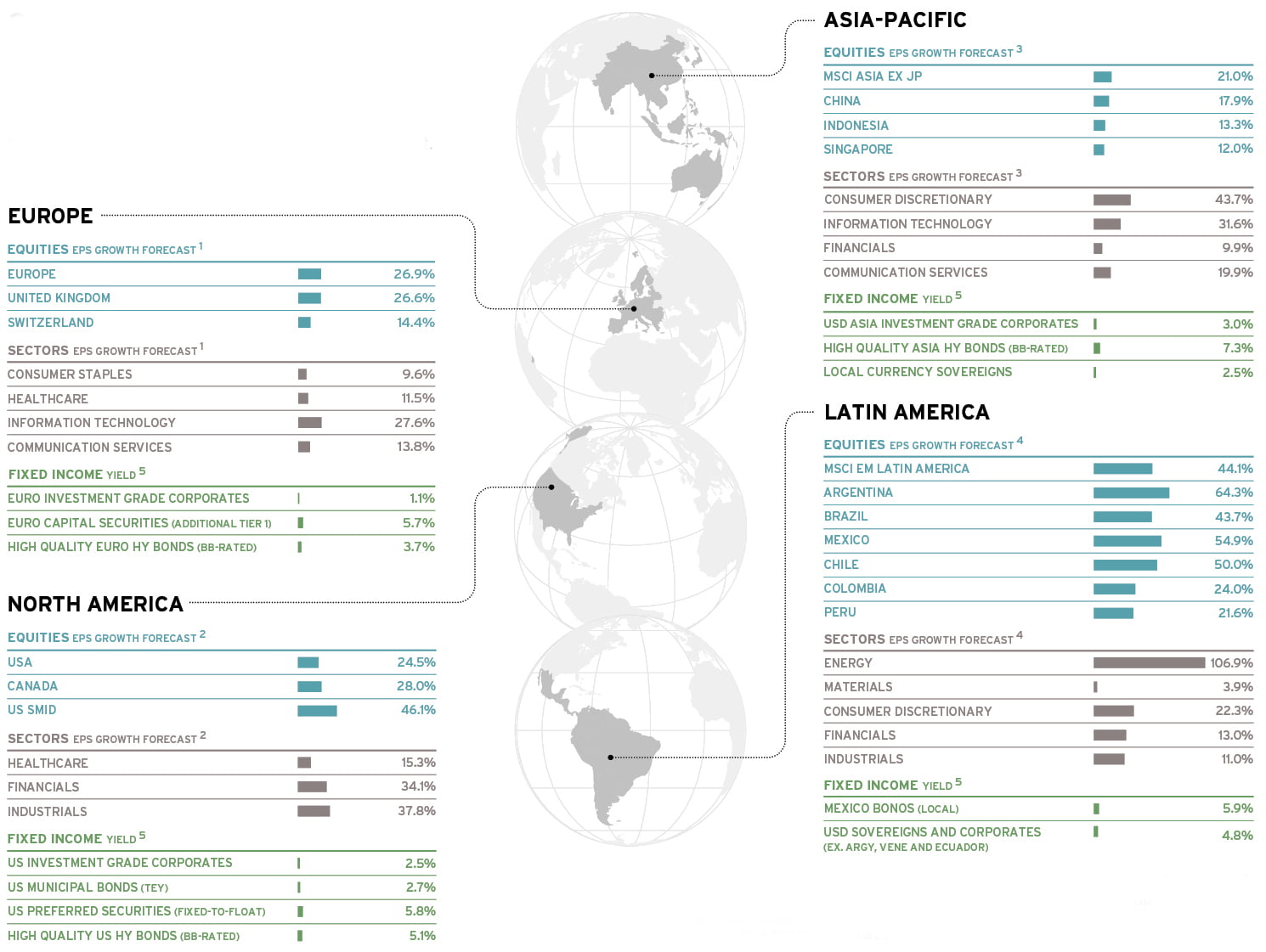

We want to reiterate our conviction in our Unstoppable trends. These include Digital disruption – such as digital media content, e-commerce, and cybersecurity providers – and Increasing human longevity – global healthcare. China and the US have led major global equity markets, and we are overweight both. Importantly, these markets have the highest weightings in COVID-defensives – figure 6. Asia, as a whole, remains an Unstoppable trend for reasons that are eminently clear, including accelerating demographics and the changing geopolitical environment.

Source: Bloomberg through 5 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only COVID cyclicals: Financials, industrials, energy, materials, real estate, consumer discretionary ex-Amazon COVID defensives: IT, healthcare, communication services, consumer staples, utilities, Amazon

Of course, in this new cycle, those assets we classified as “unstoppable” performed well relative to others in the COVID collapse. We therefore remind investors that assets whose prices have not fallen cannot rebound. Consequently, we advise you to retain these assets for the long term, while tactically adding to beaten-down sectors in the near term.

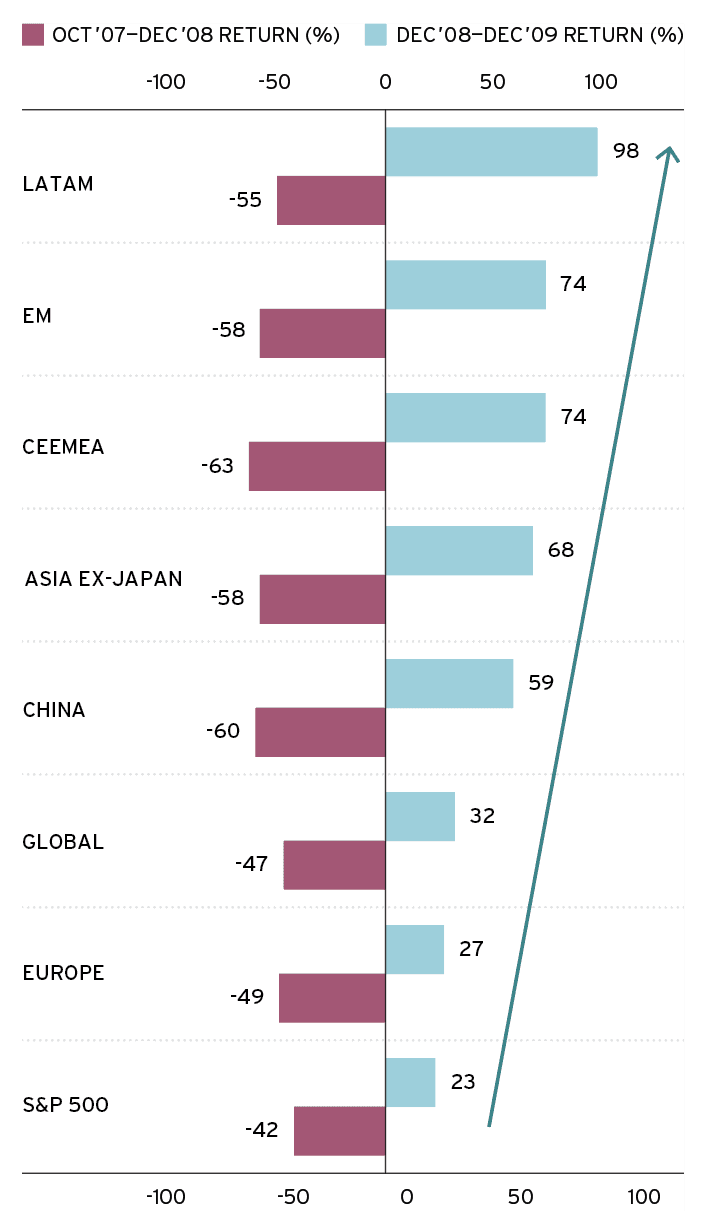

Among the underperforming “COVID cyclicals,” we see higher probability that US small- and mediumsized firms experience a quicker and more decisive rebound. Meanwhile, valuations in Latin America – 2020’s worst regional performer to date – appear to have suffered a much deeper de-rating than other EM regions. But we should recall that Latin American equities posted a 98% gain in US dollars in 2009.5 Their 2008 decline barely exceeded this year’s drop thus far – figures 7 and 8.

MSCI Indices in all cases, except for S&P. Source: Bloomberg, as of 5 May 2020. Source: Bloomberg, as of 5 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. See Glossary for definitions.

MSCI Indices in all cases, except for S&P. Source: Bloomberg, as of 5 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only

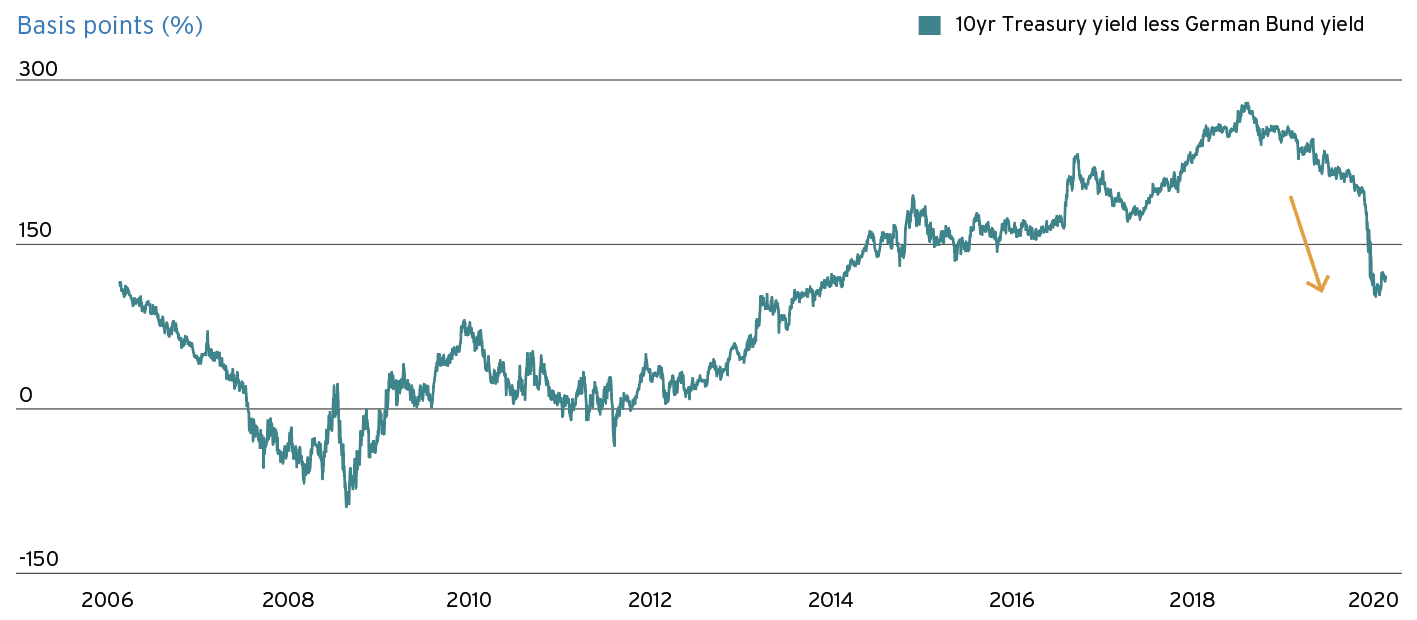

Our regional preference to overweight US bonds – with Europe and Japan already negatively yielding and “priced for crisis” before COVID-19 – remains a key position. Fed easing has again resulted in sharply lower yields across the US Treasury yield curve, despite record US borrowing.

Real US government bond yields are significantly negative, largely closing the gap with negative European and Japanese nominal yields – figure 9. But with long duration US Treasury prices surging as much as 40% over the past year, we have pared back to a neutral weighting. With 10- to 30-year yields now ranging from 0.65% to 1.30%, we see US Treasuries now solely as a risk hedge rather than an income source – see Cash is not king.

The plunge in cash interest rates and bond yields represents the key asset allocation dilemma of the future, with US real yields now negative too. Credit instruments can eke out positive real returns, but generally proportional to their default risk. Credit’s potential to substitute for sovereign credit in asset allocation looks increasingly suspect – see Towards a new asset allocation.

Source: Bloomberg, as of 5 May 2020. Past performance is not indicative of future returns. Real results may vary.

What you need to do in the new cycle

Today’s new cycle in the economy and markets is already markedly different from many past cycles. The recent rapid advance in equity markets is unprecedented, coming so soon after the most devastating economic event in the past century. As the world transitions from fear to prosperity, we now advise you to follow a post-pandemic asset allocation. Rates are low and are going to stay low. That requires considering how to manage your cash more wisely, and how to create less reliance on fixed income for diversification. We also believe that the choice of equity exposures and the sequencing of how and when to invest will be essential. Further, with so much dispersion occurring in the aftermath of COVID-19, we must position portfolios to take advantage of this dispersion and the mean reversion that is likely to occur. As this new recovery cycle continues to advance over the coming years, we expect to adopt a greater risk-taking posture reflecting the expected and unexpected opportunities that will most certainly arise.

1 China Association of Automobile Manufacturers, as of 1 May 2020 2 Bureau of Economic Analysis and Eurostat, as of 1 May 2020 3 All forecasts are expressions of opinion and are subject to change without notice and are not intended to be a guarantee of future events. 4 Diversification does not ensure against loss. 5 Past performance is not indicative of future returns.

LONG-TERM GROWTH OPPORTUNITIES LINKED TO OUR UNSTOPPABLE TRENDS OF DIGITAL DISRUPTION, THE RISE OF ASIA, AND INCREASING HUMAN LONGEVITY

COVID-CYCLICALS: SECTORS WHOSE BUSINESSES WERE STRUCK HARDEST DURING THE PANDEMIC

CAPITAL MARKETS STRATEGIES THAT SEEK INCOME FROM VOLATILITY AS WELL AS THE POTENTIAL TO BUY EQUITIES AT LOWER LEVELS

PRIVATE EQUITY AND REAL ESTATE MANAGERS THAT TARGET STRESSED AND DISTRESSED ASSETS

HEDGE FUNDS THAT SEEK TO TAKE ADVANTAGE OF LIQUIDITY STRAINS AND FORCED SELLING

DIVIDEND GROWERS WITH RESILIENT BUSINESS MODELS FROM CERTAIN INDUSTRIES

Citi Private Bank, as of 20 May 2020

*Factors in non-US Developed Market Investment Grade underweight

As we enter the new cycle, we are overweight emerging market (EM) equities, developed small- and mid-cap equities, as well as US sovereign fixed income and EM debt.

1 - MSCI, FactSet as of 7 May 2020; 2 - Factset as of 20 May 2020; 3 - FactSet as of 10 May 2020; 4 - Bloomberg as of 10 May 2020; 5 - Bloomberg and Bloomberg Barclays Indices as of 6 May 2020. Past performance is no guarantee of future returns. Real results mayvary. Indices are unmanaged. An investor cannot invest directly in an index. All forecasts are expressions of opinion and are subject tochange without notice and are not intended to be a guarantee of future events