PHIL WATSON, HEAD OF THE GLOBAL INVESTMENT LAB

Our rigorous analysis shows that investing immediately has produced better results four‑fifths of the time. Less cash and less waiting is a potent portfolio booster.

KEY MESSAGES

Despite our advice, there has been a recent increase in many clients’ cash levels. Some routinely hold as much as 35% cash in their core portfolios.

If you are currently holding excess cash, you may well be wondering when and how to invest it. With so much uncertainty over the post-pandemic economic outlook, you may feel tempted to await the next market correction before making your move. Likewise, you might be split over whether to invest all your cash in one go or in stages.

Fear of experiencing regret later on is likely a powerful influence on your thought process. However, we recommend that you base your decision on certain key lessons drawn from decades of financial market history.

Staying out of the market is costly. We compared the performance of a fully invested globally diversified portfolio and a cash-heavy portfolio between 1955 and 2020.1 Breaking this era down into rolling five-year periods, we note that globally diversified portfolios outperformed cash-heavy portfolios 97% of the time. Over that 65-year period, there was no five-year window during which the globally diversified portfolio lost money.

The market’s best and worst days cluster tightly. Some of the stock market’s best days often follow its worst days closely. Between 24 February and 1 April 2020, the S&P 500 registered eight of its worst ten days in the last decade. But it also experienced seven of its ten best days for the same period.

Without those best days, the last four months’ total return would have been -42%, instead of -9%. This is the typical pattern around periods of market stress. Between 2000 and 2020, 70% of the S&P’s top twenty best days occurred within a month of one of its worst days. Being out of the market at times like this can do lasting damage to your wealth.

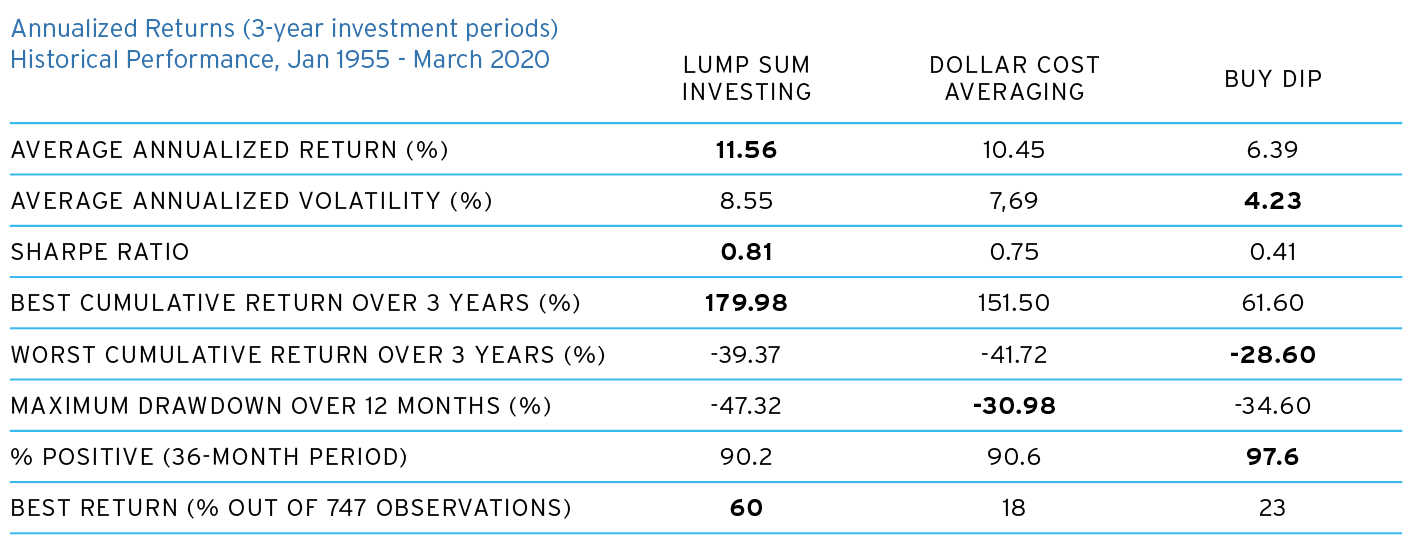

Having decided to invest, the next question is whether to commit all your cash all at once or in stages. We compared core developed equity portfolios following three entry strategies: investing all at once (“lump sum investing”), investing in five equal installments (“dollar cost averaging”), and buying only when the market drops by a certain amount (“dip buying.”) Exploring three- and five-year holding periods from 1955, we found lump sum investing achieved higher absolute and risk-adjusted returns than the other two strategies – figure 1. Investing immediately produced higher subsequent returns 80% of the time, even during bear markets.

Source: Global Investment Lab, Citi Private Bank, as of 1 May 2020. Asset classes analyzed are Developed Equities and Cash. Dollar cost averaging and “buy the dips” strategies include interest from cash. Lump sum investing: assumes entire amount invested at the outset. Dollar cost averaging: the investments are made over a horizon of twelve months, in five equal investments. Buy the dips starts with 100% cash. Throughout the three-year investment periods, one-third of the available amount is invested whenever the market drops by 7.5%, otherwise stay in cash. Past performance is no guarantee of future returns. This analysis does not include commissions and/or fees that would have reduced the performance shown. See Glossary for definitions.

We believe the evidence of history is clear. If you are holding excess cash, you should put it to work in a globally diversified core portfolio as soon as possible. You should then keep it fully invested for the long term. Let us help you do so.

1 Global allocation: AVS Level III + Hedge Funds. Simulated historical returns are based on asset class returns using indices as a proxy and should not be considered a guarantee of future performance. Global allocation: using AVS time series Global USD Level 3: Global Developed Equities 47%, Global Emerging Equities 7%, Global Developed Investment Grade Fixed Income 27%, Global Developed Corporate High Yield Fixed Income 2%, Emerging Market Fixed Income 2.2%, Cash 2%, Hedge Funds 12%. Allocation is rebalanced annually. Performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index. The aforementioned illustration does not reflect the deduction of any fees or expenses. The illustrations use data from 1 Jan 1950 to 20 Mar 2020.