STEVEN WIETING, CHIEF INVESTMENT STRATEGIST AND CHIEF ECONOMIST

Achieving diversification by combining equity and fixed income has become much harder. This requires us to consider additional opportunities for building globally diversified portfolios.

KEY MESSAGES

Build a globally diversified core portfolio and keep it fully invested for the long term. There is perhaps no more important piece of investment advice that we could offer you as your trusted partners – see Our Investment Philosophy and Process in Outlook 2020. Over time, this advice has helped to protect and grow wealth more effectively than any other single approach. We believe that it will continue to do so. At the same time, changes in the returns and greater risks associated with certain asset classes make achieving diversification more challenging than ever before. We therefore need to rethink aspects of our asset allocation.

Less risk takes more effort

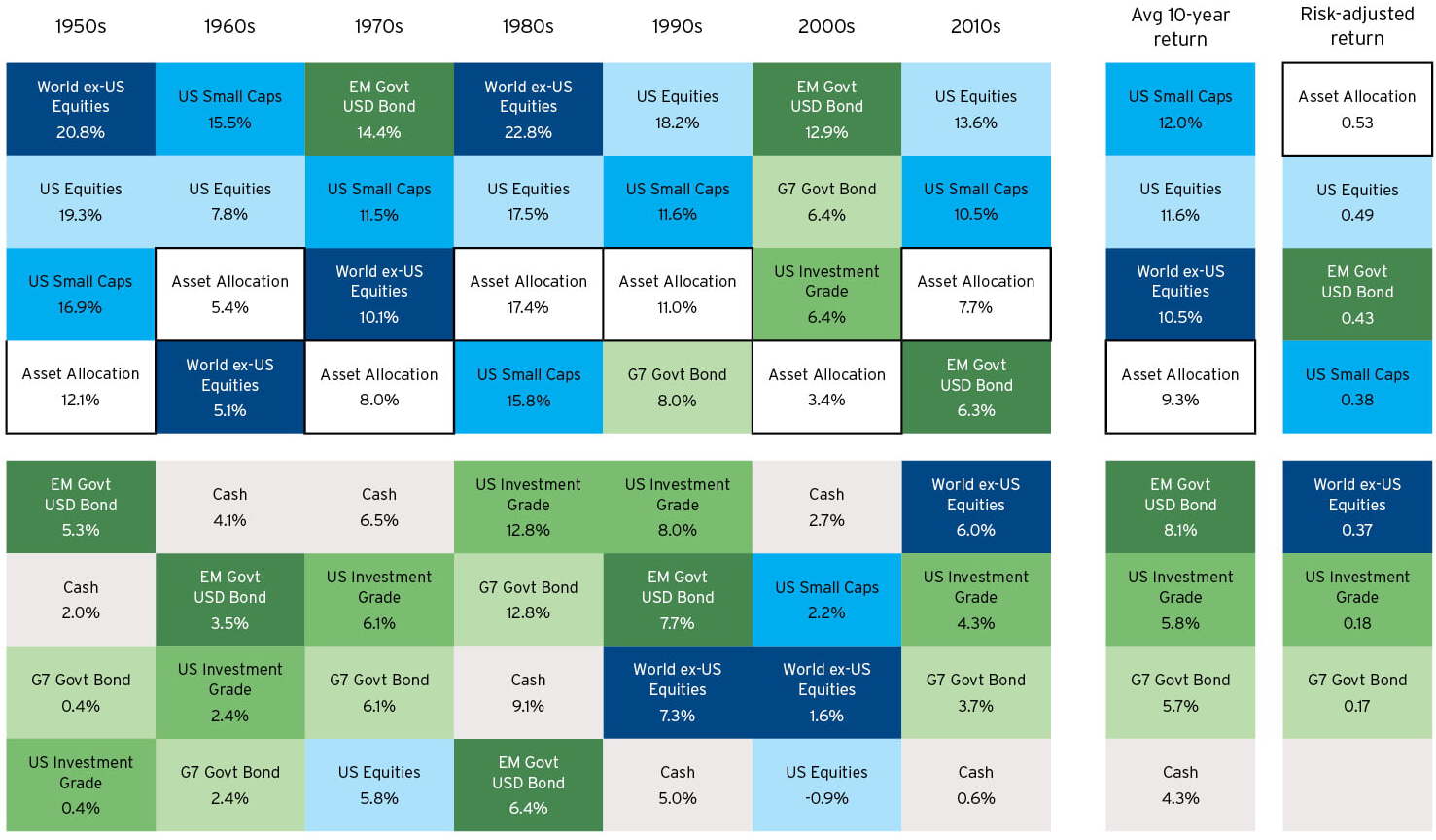

In investment, there is no such thing as an entirely free lunch. Diversification is perhaps the next best thing to it. A globally diversified asset allocation has produced superior risk-adjusted returns relative to every individual asset class between 1950 and 2020 – figure 1.

Source: FactSet and Citi Private Bank, Global Asset Allocation team as of 20 Apr 2020. Adaptive Valuation Strategies (AVS) is the Private Bank’s proprietary strategic asset allocation methodology. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. Past performance is no guarantee of future returns. Real results may vary. “Asset allocation” in this diagram represents an AVS Risk Level 3 allocation, which includes allocations to equities, fixed income, commodities, cash and hedge funds. Risk levels are an indication of clients’ appetite for risk. Risk Level 3 – Seeks modest capital appreciation and, secondly capital preservation. The returns shown were calculated at an asset class level using indices and do not reflect fees, which would have reduced the performance shown. Risk-adjusted return is defined here as the Sharpe ratio. See Glossary for definition of terms.

Combining equities and fixed income, as well as other asset classes, in the appropriate proportions, dampens portfolio volatility over time. When equities have fallen sharply, high quality fixed income assets have typically risen. The strongest rationale for those gains is the assured income that those bonds provide. However, as yields have fallen and bond income has become scarce, the shortterm and long-term diversification properties of bonds fade.

The global yield for all developed and emerging market bonds of all qualities – including subinvestment grade – is now just 1.4%. Looking out several years, we believe the vast majority of fixed income assets will become “non-investments.” What we mean is that owning most bonds will be little different than holding cash. And, as we have said repeatedly, holding too much cash is a feature of market timing. It is thus likely that a portfolio with cash and a slew of extremely low yielding bonds will create a huge drag on returns over time – see The wisdom of lump-sum investing: Why you should get fully invested now.

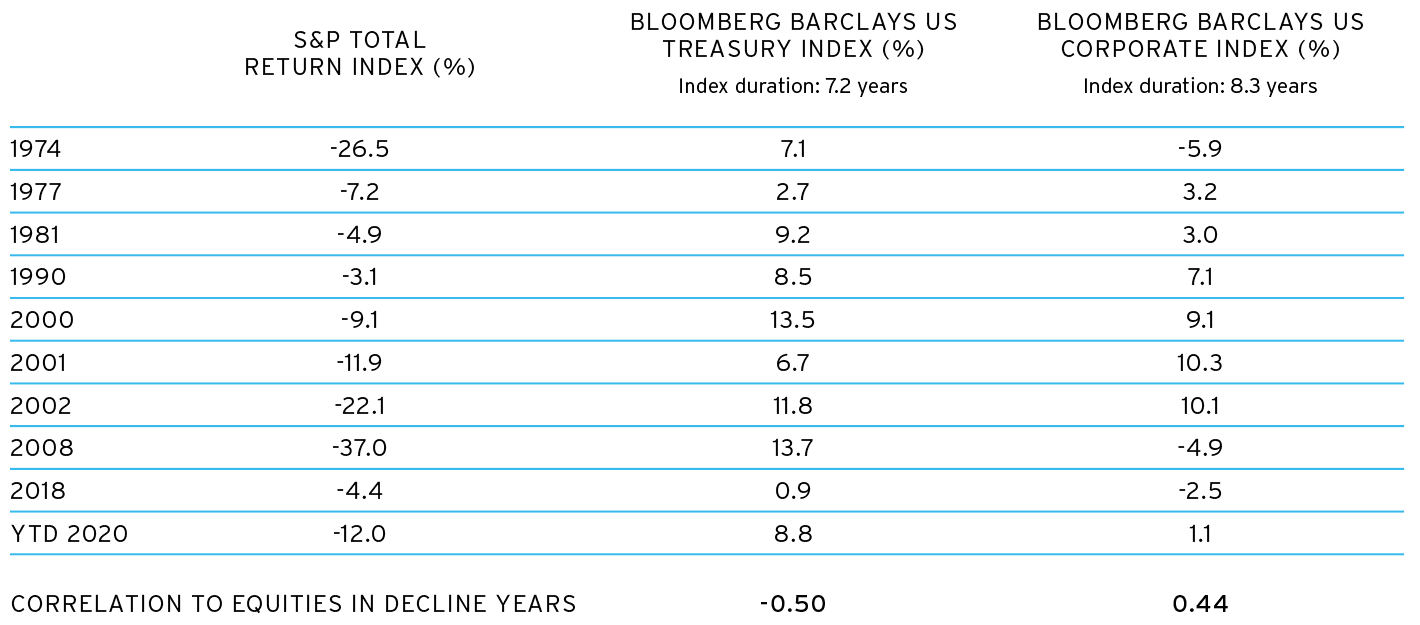

To be sure, high quality fixed income will still have a role to play in core portfolios. On the nine previous occasions when the S&P 500 Index fell over an entire calendar year, US Treasuries delivered a positive return. The correlation between Treasuries and US equities in such years was negative 0.51. In 2020 so far, this pattern has held up, with Treasuries rising as equities have fallen – figure 2. However, with 10- to 30-year Treasuries yielding only 0.65% to 1.30%, we now see them solely as a risk hedge rather than also a source of income.

Source: Haver Analytics, Bloomberg through 1 May 2020. Past performance is not indicative of future returns. Real results may vary. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only. See Glossary for definitions.

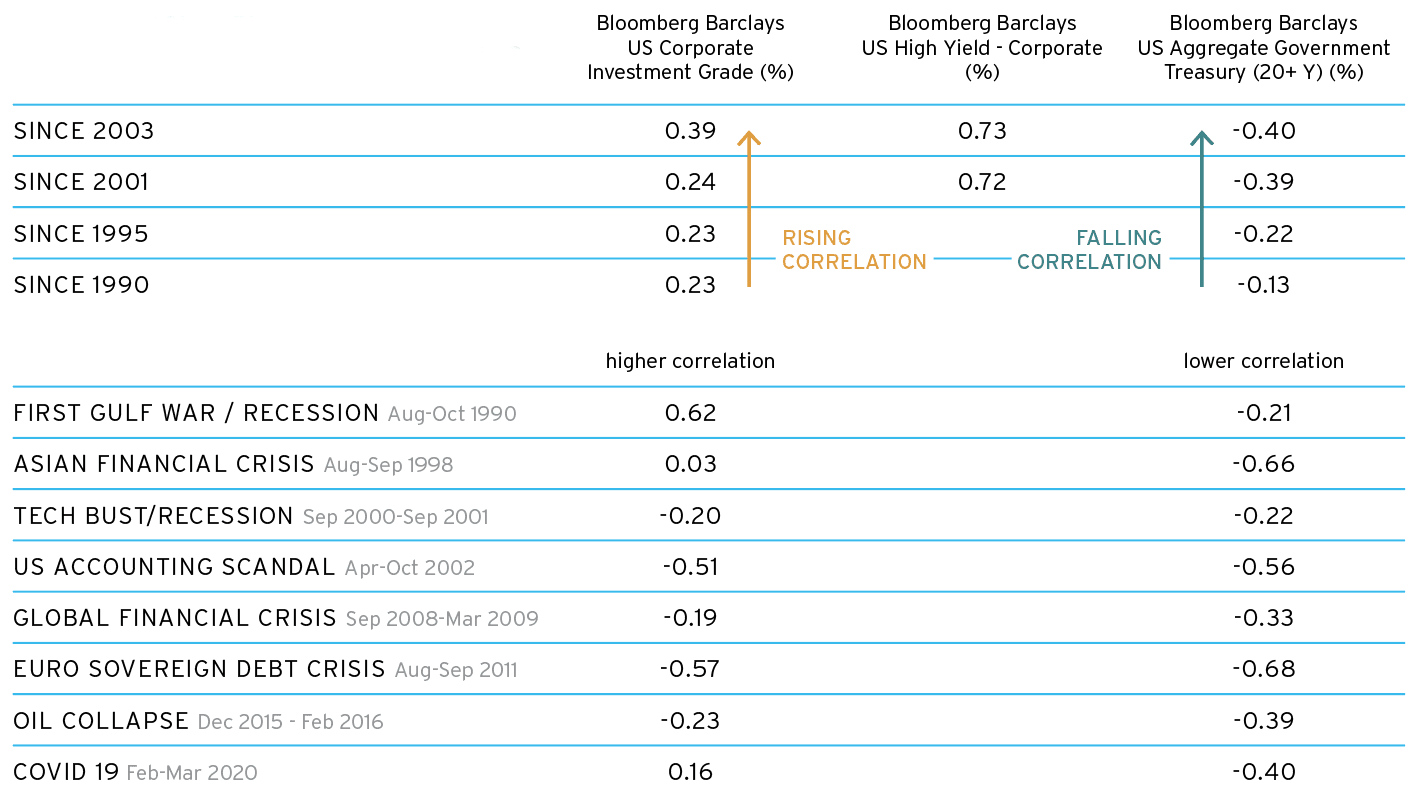

Turns out that IG credit is no substitute

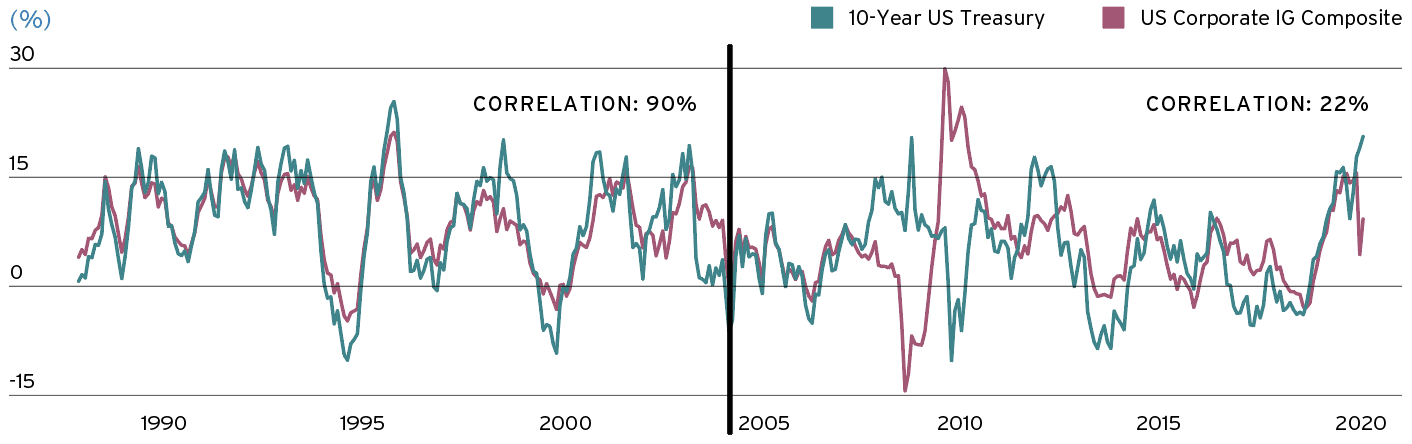

What about using investment grade (IG) corporate credit as an income-bearing portfolio substitute for Treasuries and other sovereign debt? Previously, IG corporates and US Treasuries tended to move together strongly. In the fifteen years to 2005, the correlation between their twelve-month returns was an almost perfect 0.90 – figure 3. In the last fifteen years, however, the correlation has been a much weaker 0.22. This means that IG credit is a poor risk hedge. Notably, IG credit fell during the 2008 and 2020 bouts of economic turmoil, while US Treasuries rose. Amid such severe uncertainty, investors clearly felt comfortable only with the highest quality debt of all.

Source: Haver Analytics, Bloomberg through May 2020. Past performance is not indicative of future returns.

Source: Haver Analytics, Bloomberg through May 2020. Past performance is not indicative of future returns. See Glossary for definitions. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only.

In fact, US Investment Grade credit has become increasingly correlated to equities – figure 4. Unfortunately, this is especially true during times of stress. In the calendar years when US equities have declined, the correlation between US IG corporate bonds and equities has risen to 0.45, while US Treasuries and equities were negatively correlated. Looking forward, we expect that IG credit will not deliver sufficient diversification at the times when it is needed most. One reason for this is that corporate debt and equities are typically a trade on the same entities. Corporate debt is higher in the capital structure, relatively safer than equity, but with a much more limited potential return.

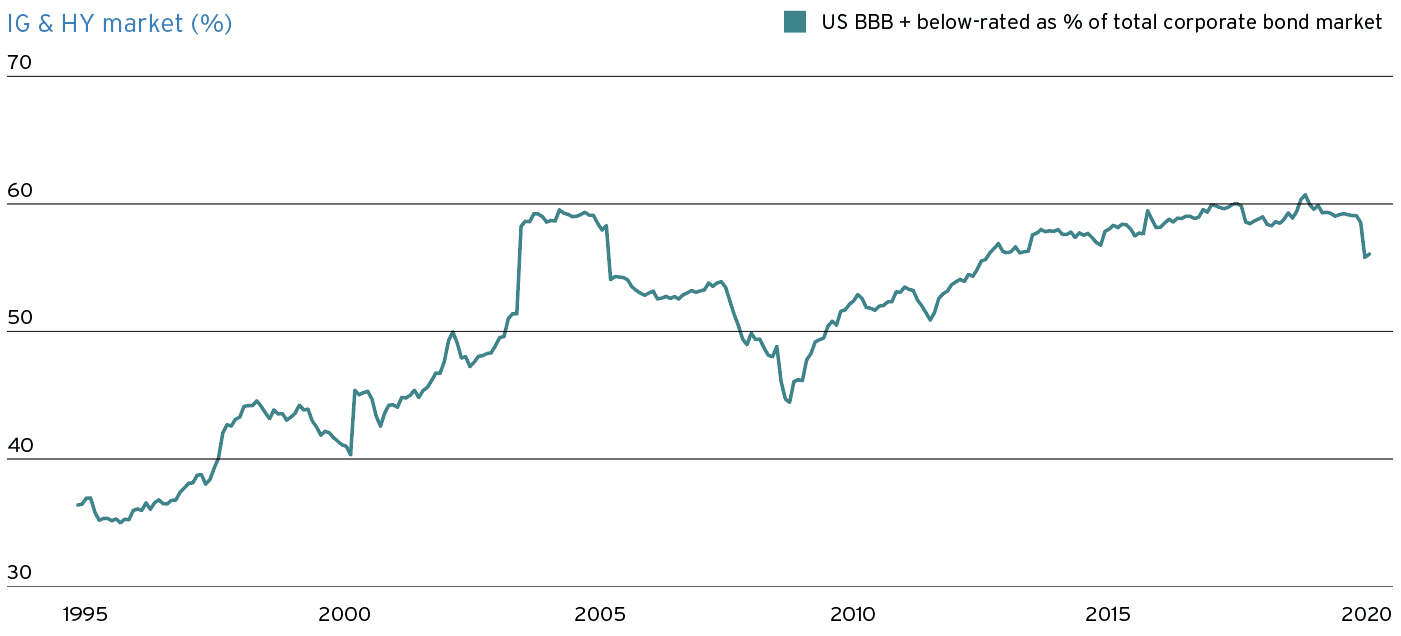

A second important reason for the rising equity-credit correlation is the growing indebtedness of the US corporate sector. Average credit ratings have declined through the last economic expansions. One symptom of this is the rise in the proportion of US debt rated at BBB – the lowest IG rating – and below – figure 5. Developed market corporates outside the US do have relatively stronger balance sheets. However, these generally come with lower yields.

Looking abroad, we see that emerging markets corporates are no substitute for large sovereign borrowers. While still a worthwhile asset class on their own, neither foreign companies nor their home governments have access to a printing press in US dollars or other reserve currencies. They cannot therefore substitute for IG Credit in US dollars.

IG debt, therefore, cannot provide the income and diversification we have previously received through its inclusion.

This is a major change to asset allocation and one that must be taken very seriously.

A new asset allocation

In today’s uncertain world of record low interest rates and yield, the quest for core portfolio diversification is both more vital and more challenging than ever. We must look for substitutes for some traditional holdings in the quest to create better long-term risk-adjusted returns.

One consideration is gold. Over the past three decades, the yellow metal’s annual returns have shown little correlation with developed market equities. Crucially, it can provide diversification during times of equity stress. Despite broad-based liquidations during the worst of the pandemic-driven sell off of 2020, its spot price dipped just to where it started the year while US equities were down 35%. That said, of course, gold’s disadvantage is that it pays no income whatsoever. While gold can help hedge core portfolios, therefore, it plainly cannot substitute for income-bearing diversifiers.

Other considerations include dividend equities. However, these still have correlations with other equities that are too high to provide meaningfully greater diversification. Preferred equities also provide small portfolio benefits. Alternative investments are, therefore, likely to become increasingly important to diversified long-term portfolios.

Private equity will be a beneficiary of low interest rates for years to come. Similarly, latestage venture capital strategies take on less equity risk by gaining exposure to companies at lower valuations, before they are public. In all of these cases, though, the historical benefits of Treasuries cannot be replicated.

Looking ahead, we would highlight the potential of capital markets strategies. For suitable clients, these may represent an opportunity to create elements of equity and fixed income allocations. Implied volatility has two basic regimes, one high and low. When volatility surges, strategies exist that seek to generate income – see What smart families are doing in capital markets. When volatility is low, hedging costs are low, enabling diversification to be added cheaply to core portfolios. In time, we believe hedges and income strategies in place of some bonds will become critical elements in the “new asset allocation.”

To see how well your core portfolio is currently diversified, ask us for your own personalized Outlook Watchlist report. We can then suggest customized opportunities to help enhance your asset allocation.

Joe Fiorica and Joe Kaplan also contributed to this article.

1 See Glossary for definition.